Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

I want to start with something that irritated me this weekend.

Yahoo Finance ran a piece arguing that AI stocks need to split so retail investors can participate. The author’s point was essentially this: stocks at $500, $900, $1,600 a share are shutting out Main Street, and companies have a responsibility to split.

That’s the wrong message. And I’m going to tell you exactly why — and why it’s connected to the same bubble narrative that keeps resurfacing every few weeks.

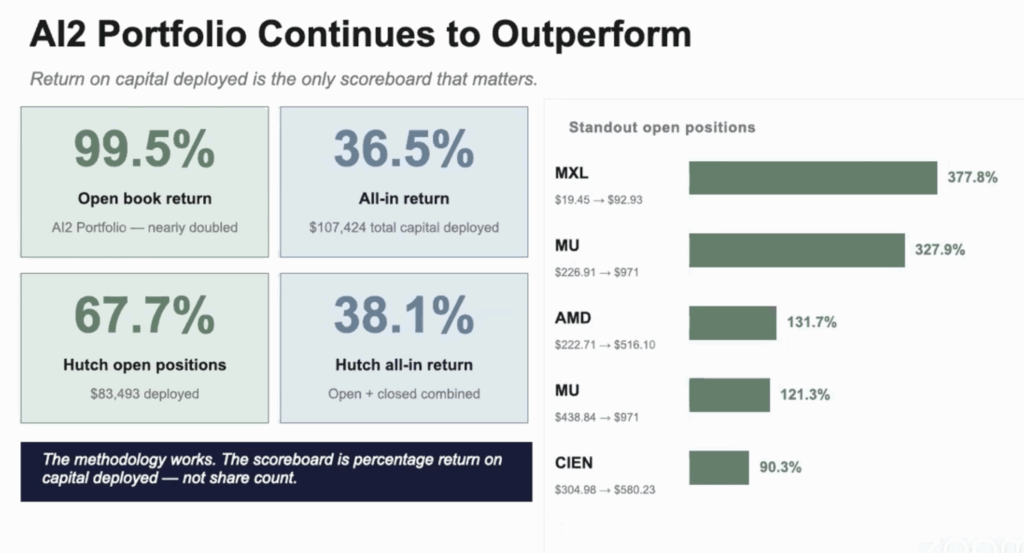

But first, the number that matters this morning: the AI2 open positions portfolio is sitting at 99.5% return since February. AMD has more than doubled since the beginning of April. Micron and MaxLinear are both well over 300%. And a portfolio of just six stocks I shared at the IBL conference in March is up 49.4% in 60 days on roughly $11,000 invested.

The bubble people keep saying the same things. The tape keeps saying something different.

Stock Splits Don’t Create Value. Here’s What Does.

The article that set me off this weekend was written by Brian Sozzi at Yahoo Finance. A viewer named Dorothy wrote in asking why top AI names trading at $500 to $1,000 aren’t splitting — because the market is “shutting out Main Street.”

I understand the frustration. I really do. But splits don’t create value. They have nothing to do with the fundamentals of a company. When Priceline split 25-for-1 last month — the first split in the company’s history — the stock went from roughly $4,000 to about $20 a share. The number of shares changed. The business didn’t.

Here’s the real point Dorothy and the author are missing: price is not the problem. Capital is the problem. And that’s a very different conversation.

If you can’t afford one share of a $900 stock, that’s a money issue — driven by four years of inflation, rising gas prices, and increasing pressure on the middle class. That’s real, and I’m not dismissing it. But the solution isn’t stock splits. The solution is understanding that you don’t need 100 shares of something to profit from it.

We bought five shares of Micron at $438. Just five. That position is up over 120%. One share of SanDisk at $1,600 — if it reaches its raised price targets of $3,200 — is a $1,600 gain and a 100% return. One share. The quality of the company is more important than the number of shares you can afford to own. Always.

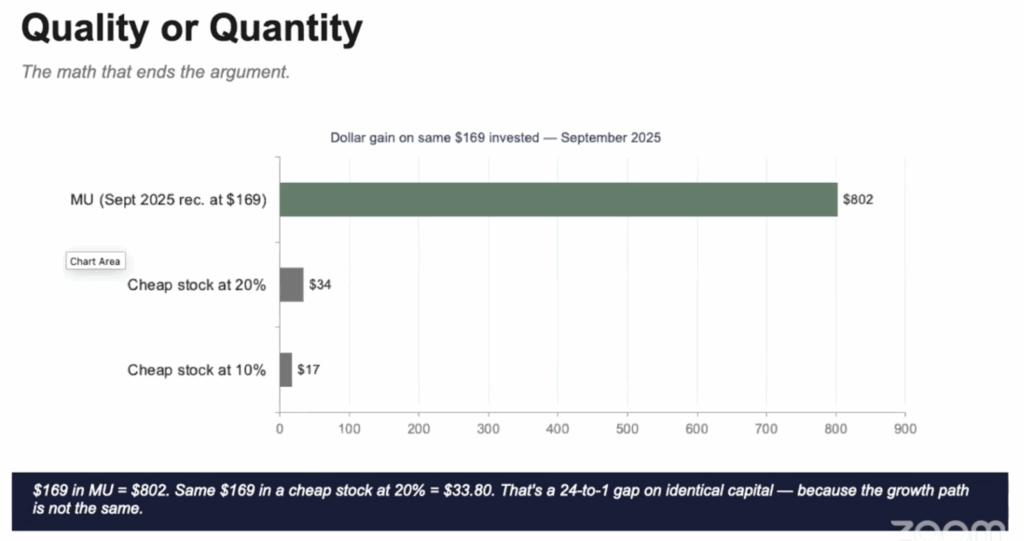

The math ends the argument: $169 invested in Micron at our September recommendation price produced an $802 gain. The same $169 in a cheap stock that returned 20% produced $34. That’s a 24-to-1 gap on identical capital — because the growth path is not the same.

And here’s something else worth knowing: there are specific reasons why many of these companies aren’t splitting right now. When Nvidia invests in Lumentum and receives warrants for share ownership in return, neither company wants those warrants to be worth less than the value at the time of the deal. Splits would require rewriting agreements. They also don’t want extreme volatility in share prices when they’re using stock-based valuations to justify debt arrangements. The no-split environment isn’t an accident. It’s strategic.

Looking Back: What the AI2 Summit Got Right

In September of last year, I held the first AI2 summit and shared five stock recommendations. I want to revisit them honestly — the wins and the misses.

Micron: up over 470% since I recommended it. Their HBM3 memory was already sold out when I presented it last September. Now their memory is sold out through 2026, 2027, and into 2028. The thesis hasn’t changed. It’s just gotten more confirmed with every passing quarter.

Applied Optoelectronics: up over 400%. Optical demand was the thesis then. It’s even more obvious now.

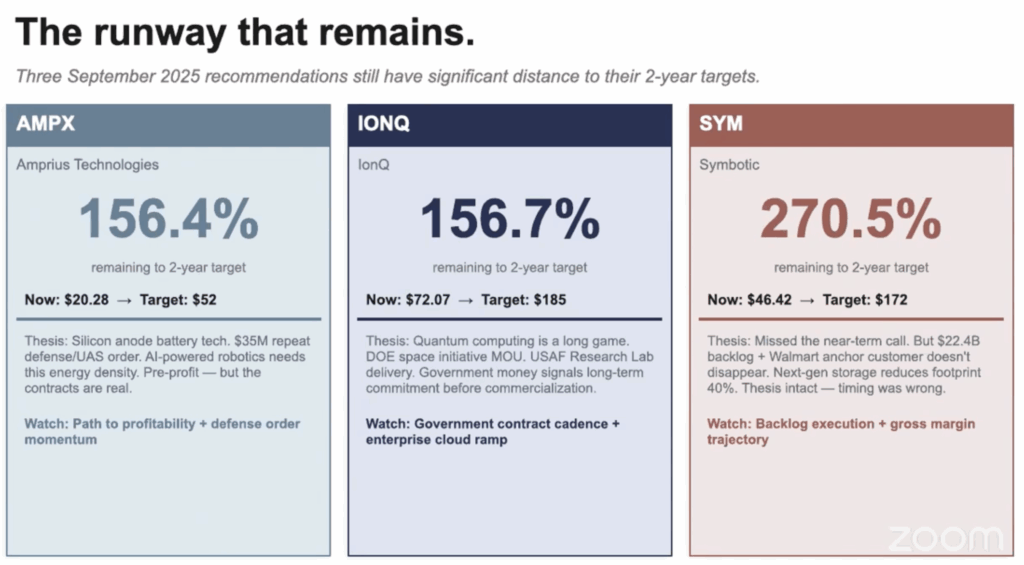

Amprius: up over 70%. We still hold this one. Current analyst targets are running $40–$52 a share versus a current price around $20. It’s a battery company finding its way into AI, space, drone, and quantum computing applications. Significant institutional accumulation in the last two months. The growth runway is real.

IonQ: essentially flat, then caught a momentum run on Pentagon funding news. Quantum computing is the future — but it’s still too speculative. Watch for the momentum run, pullback pattern. That’s their cycle.

Symbiotic: down 18% since the September recommendation, though it had a high in the 70s in between. The risk I flagged was single-client concentration — they’re largely dependent on Walmart. I was wrong on timing. The thesis may still be intact.

The lesson across all five: the process works when the fundamentals are there. Micron and AAOI were deeply undervalued relative to their forward earnings at the time. The market repriced them because the earnings proved the thesis correct — faster than most people expected.

I’ll also say this: at the end of last year, Motley Fool, Porter Stansberry, and Agora all came out with Micron as their number one stock pick for 2026. We bought it in October and November of 2025. CNBC just did a big segment on Micron two weeks ago.

Y’all are late. That’s all I have to say about that.

In March at the Investors Blueprint Live conference, I gave away six stock picks: AMD, Vicor Corp, Talen Energy, Teradyne, Radnet, and Kratos Defense.

Ten shares of each — equal weight — on roughly $11,000 total.

Those six stocks are up 49.4% in just over 60 days. $5,655 dollar gain. Four of the six winners. AMD up 144%. Vicor up 76%. Two misses — Kratos and Radnet — but two misses didn’t break it. Four winners including AMD 144% did the work.

That’s the point I want you to take away from the whole stock split debate. You don’t need cheap stocks. You need good stocks. And you need to own them before everyone else figures out what they are.

The bubble talk keeps coming. Let me put it to bed one more time.

The 1999 dot-com crash had a specific cause: IPO mania. Over 450 IPOs in 1999 alone. The majority had nearly 100% returns on their first day. Retail investors, newly equipped with online trading accounts, poured hundreds of millions of dollars into companies with no revenue, no earnings, and no business model.

Nvidia earns $40 billion a year. Its customers are the most profitable companies on Earth. That is not Pets.com.

And here’s the other thing the bubble crowd keeps ignoring: the dot-com crash was a consumer crash. Consumers tried to use the internet and found it didn’t work well enough yet. The products weren’t ready.

This AI buildout is a business transformation. Businesses are investing in and adopting artificial intelligence faster than expected. The demand is coming from enterprise. That’s an entirely different economic dynamic.

And the demand extends further than most people price in. Right now we’re in cloud inference — big data centers, hyperscaler spending. But edge inference is coming. AI running locally on devices, at the network edge — and it requires an entirely new layer of infrastructure. Every segment of the supply chain gets paid again.

These companies can’t keep up with demand as it stands today. Their order backlogs extend into 2027 and 2028. The build-out isn’t ending. It’s multiplying.

What’s Coming This Summer

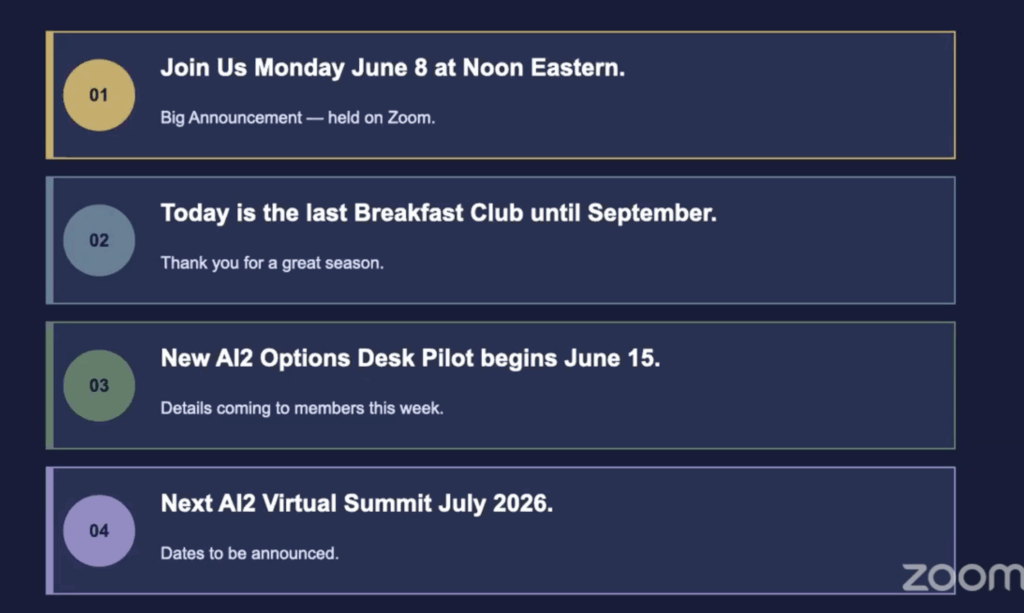

This is the last Breakfast Club until September. I may drop in for a couple of special sessions during the summer as things develop, but no set schedule.

Monday June 8th at noon Eastern: big announcement on Zoom. Mark your calendar.

June 15th: the AI2 Options Desk Pilot begins. Details going out to members this week.

July 2026: the next AI2 Virtual Summit. I’ll announce the date around the 4th of July weekend. What I can show you at that point is everything that has changed in artificial intelligence from last September to today — how the universe of stocks is evolving and where the next opportunities are being priced too low right now.

The AI2 index across 356 stocks is up 23.6% for the year. The supply chain and core segments continue to lead. The thesis keeps proving out.

Don’t let the bubble talk shake you. And don’t let anyone tell you that cheap stocks are better than good stocks.