Welcome to the Breakfast Club, your weekly dose of market insights and trading strategies! Join us live every week at 9 AM ET on Traders Reserve Live, where John Hutchinson breaks down the latest market movements, shares actionable trade ideas, and answers your most pressing questions.

Michael Burry has over a billion dollars in Nvidia puts.

Mark Westenberg appeared on CNBC this weekend calling AI infrastructure a bubble. Ray Dalio chimed in. The bear case on artificial intelligence is back, louder than it’s been in months, and it’s timed perfectly to land the week before Nvidia reports earnings.

I read every word of their argument. And I want to walk you through exactly where they’re right, where they’re wrong, and why their biggest mistake isn’t the conclusion — it’s what they refuse to look at.

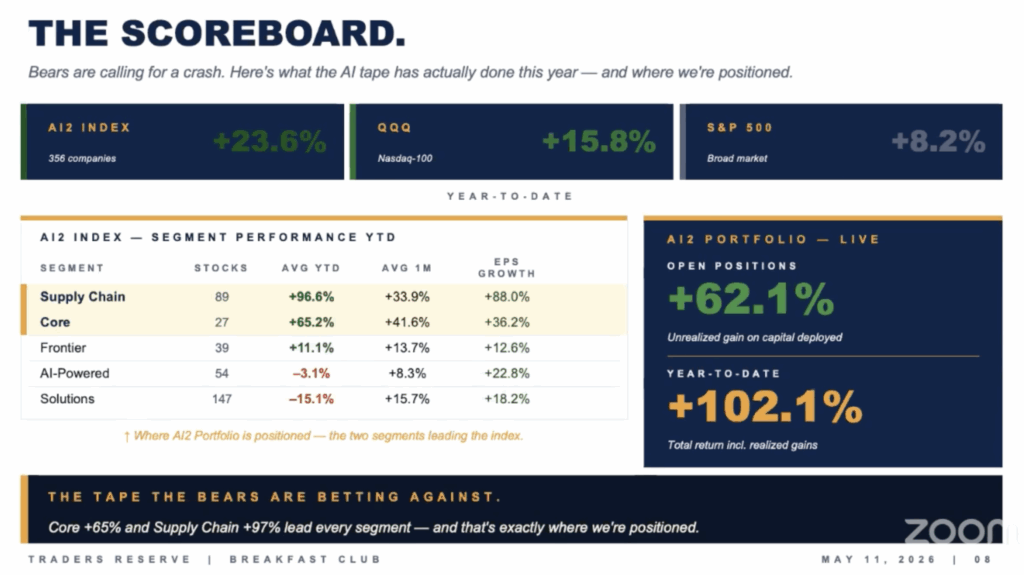

But first, the number that matters this morning: the AI2 portfolio just crossed 102% year to date. $35,000 is now worth more than $70,000. We did it without owning Nvidia, Microsoft, Meta, or Amazon. We did it owning the companies that supply them.

Let’s talk about why the bears are missing that entirely.

What the Bear Case Actually Says

The argument has five pillars. I’ll give them a fair hearing — because one of them is actually legitimate.

Customer concentration. Nvidia’s top four customers account for 61% of revenue. Two customers account for 37%. This is a real risk. But here’s what the bears don’t say: those four customers are Google, Microsoft, Meta, and Amazon — the same companies that just raised their combined 2026 AI capex to $650–$725 billion. That’s not a fragile customer base. That’s the entire engine of the buildout.

Capital expenditure concerns. The bears say too much money is being spent. But Microsoft attributed roughly $25 billion of their capex increase directly to component pricing — meaning suppliers can’t keep up with demand. That’s not reckless spending. That’s a supply problem.

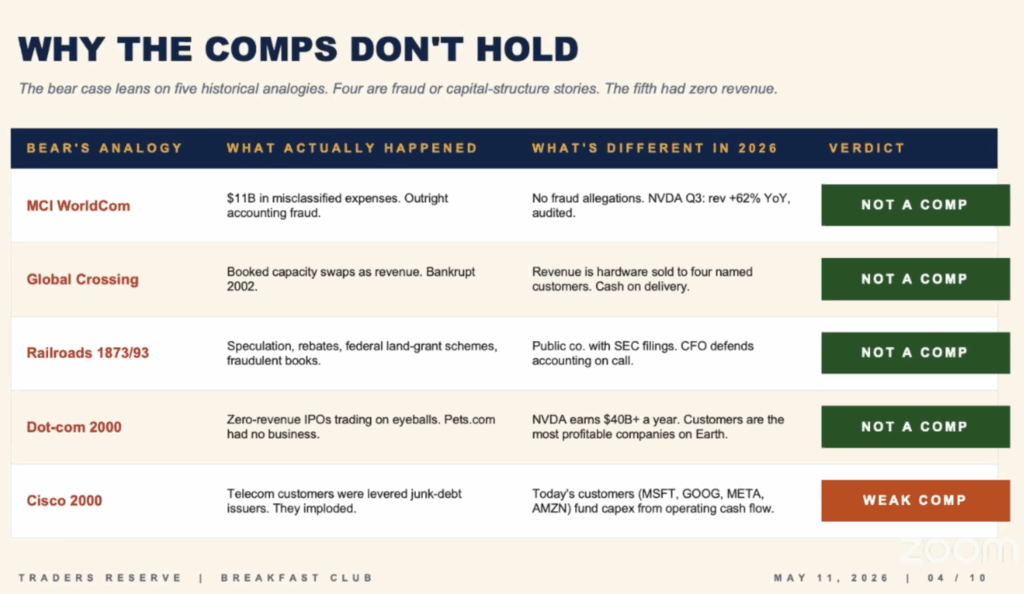

Asset life mismatch. This is the accounting argument — that the way hyperscalers are depreciating their hardware is similar to how MCI WorldCom faked its buildout data. Nvidia’s Q3 revenue was up 62% year over year and audited. Revenue is hardware sold to four named customers. Cash on delivery. Not a comp.

Substitution risk. This one is legitimate. At some point, Nvidia will face real competition — TPUs, Trainium, MTIA are already in development. The question is when, and the bears treat it as imminent when the evidence doesn’t support that timeline.

Circular financing. Nvidia owns equity stakes in customers and has committed $860 million in lease guarantees. The bears call this off-balance-sheet risk. I call it investing in your own supply chain when supply is the bottleneck. Nothing illegal about it.

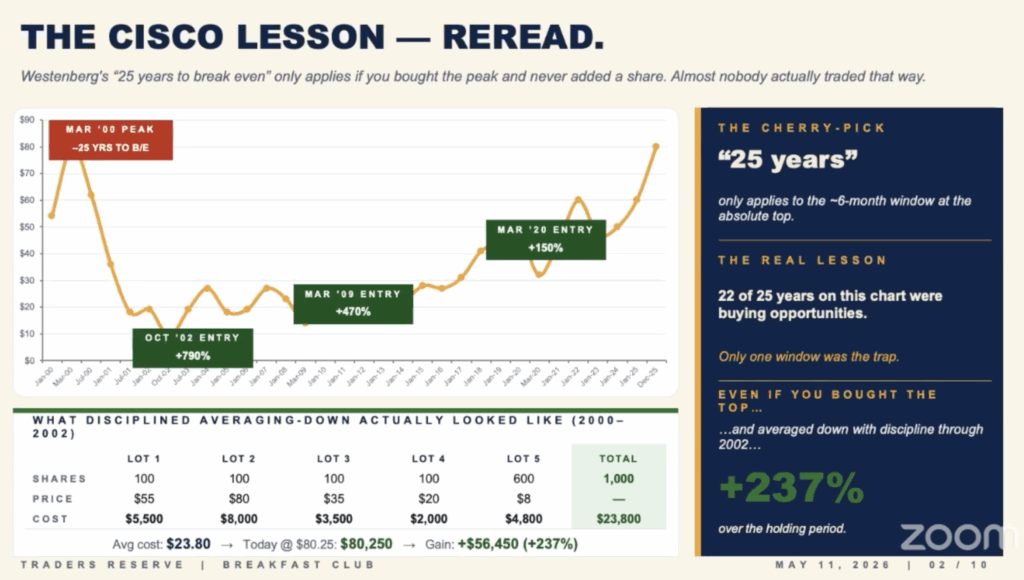

The Cisco Comparison That Doesn’t Hold Up

Westenberg’s headline argument: if you bought Cisco at $80 in 2000, it took 25 years to break even.

He’s right about that specific scenario. But here’s the trap: it only works if you assume everyone bought at the all-time high and never added a share. That’s not how investors work.

22 of the 25 years on the Cisco chart were buying opportunities. Only one window was the trap. If you bought at $80 and averaged down with discipline through 2002 — adding at $55, $35, $20, and loading up at $8 — your average cost was $23.80. At today’s price, that’s +237%. Same stock. Same 25-year window. Completely different outcome.

And more importantly: Cisco’s customers in 2000 were leveraged junk-debt issuers. They imploded. Today’s customers fund AI capex from operating cash flow. Westenberg uses the same ticker symbol and calls it the same story. It isn’t.

MCI WorldCom: $11 billion in misclassified expenses. Outright accounting fraud. Not a comp.

Global Crossing: booked capacity swaps as revenue. Bankrupt 2002. Not a comp.

Railroads 1873 and 1893: speculation, federal land-grant schemes, fraudulent books. Not a comp.

Dot-com 2000: zero-revenue IPOs trading on eyeballs. Pets.com had no business. Nvidia earns $40 billion a year. Not a comp.

Notice the theme running through every historical comparison the bears use: fraud, fraud, fraud. None of that is happening here. When your entire bear case rests on four examples of outright fraud and one weak comparison, the case isn’t as strong as it sounds.

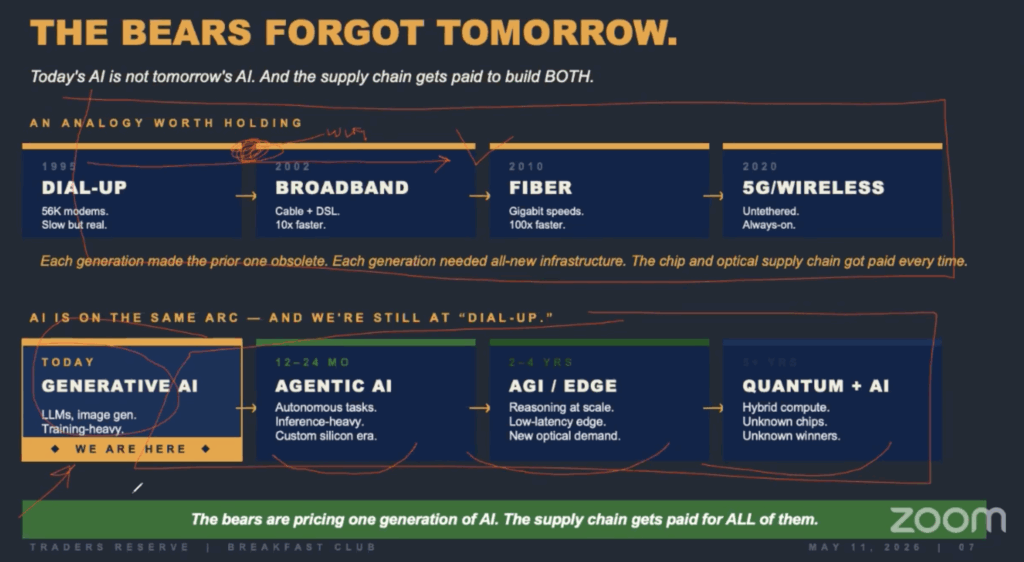

Here’s the deeper problem: they’re pricing one generation of AI and calling it the whole story.

Think about the internet. Dial-up in 1995. Broadband in 2002. Fiber in 2010. 5G in 2020. Each generation made the prior one obsolete. Each generation needed entirely new infrastructure. The chip and optical supply chain got paid every single time.

We’re at the dial-up stage of AI — right now, in generative AI. In 12 to 24 months we move into agentic AI. In 2 to 4 years, AGI and edge computing. Further out, quantum plus AI. The bears are pricing Nvidia against today’s infrastructure and ignoring the fact that every chip, every server, every optical component powering current AI will have to be replaced — multiple times — as we move through each phase.

The supply chain gets paid to build every generation. Not just this one. That’s what they’re not looking at.

What I’m Doing Instead

The bears are short one stock. We own a basket of suppliers who have already been paid.

Here’s the asymmetry: Nvidia trades at roughly 40 times trailing earnings. The bear math says if hyperscalers slow buying in Q2 2027, the forward multiple compresses 50–70% over 12 to 18 months.

But the companies we own — AMD, Micron, MXL, Broadcom, Marvell, Ciena, Coherent, Lumentum, Silicon Motion — have already booked the revenue, recognized the margin, and banked the cash. A 2027 capex slowdown doesn’t claw back 2026 sales. Their multiples are already lower than Nvidia’s. Less to compress.

Bears are betting against one forward multiple. We own twelve companies whose past quarters are already in the books.

MaxLinear is up 400% in 90 days. Micron is up 139%. Silicon Motion is up 109%. Lumentum just joined the NASDAQ 100 this week and is up 5–6% at the open today — a stock we’ve owned four separate times and currently sit on a 35% gain.

And I’ll say one more thing: Burry and Westenberg don’t offer an alternative. What do you do instead — buy gold? GameStop? If your entire argument is “don’t own Nvidia,” you owe people an answer for what to do with their money. They don’t have one. That’s the tell.

What I’m Watching This Week

The AI2 index across 356 companies is up 23.6% year to date. The QQQ is up 15.8%. The S&P is up 8.2%. The two segments leading the index — Supply Chain at +96.6% and Core at +65.2% — are exactly where the AI2 portfolio is positioned. The bears are betting against the tape that’s already printed.

Two reports this week matter. I’m not particularly worried about CPI — Wall Street already expects it to be elevated given oil prices. The market will largely look past it.

Retail sales Thursday is the one I’m watching. April is the first full month with sustained gas above $4 to $4.50 a gallon. March data held up. April will tell us whether consumers have started cutting back elsewhere. If retail sales show sustained weakness, that’s a real signal — and the one that would make me more cautious even on the supply chain names we hold.

For now: the thesis is intact. The build-out is generational. And the bears are pricing one frame of a very long movie.

AI2 briefing May 18 at 4pm. Next Breakfast Club: Monday, June 1